Venture capital plays an important role across the entire spectrum of private company building by investing in businesses at all stages of growth. Knowing how venture capital operates in the innovation ecosystem can help founders of high-growth startups acquire the funding they need.

For cash-burning tech startups with ambitious plans, acquiring venture capital dollars to fuel growth is often necessary. Navigating the venture capital landscape can be daunting, and the process of securing venture dollars is rarely straightforward. This article covers the basics of venture capital for first-time founders, as well as more nuanced topics, including:

- What is venture capital?

- Who are the key stakeholders?

- Why startups seek venture capital

- Why VCs invest in startups

- How a VC fund operates

- A typical venture capital investment process

- Expectations of startups that take on venture capital

- What startups should consider when seeking venture capital

What is venture capital?

Venture capital (VC) refers to funds that are deployed by investors, also known as venture capitalists, into select private companies (as early as pre-product and as late as pre-public) that demonstrate strong growth potential and an ability to generate a strong risk-adjusted return for investors. In exchange for their capital, investors receive an ownership stake in the private company.

“The companies (that receive venture capital) have earned conviction by way of VCs in their ability to build into a market leader, become an outlier business, and produce an outsized return as a result,” says John Rikhtegar, Vice President, Growth Capital, RBCx Capital.

Although venture capital was initially used to finance early-stage startups, the ecosystem has since matured, creating a continuous need for capital to fuel cash-burning growth. Today, VC plays an important role across the entire spectrum of private company building, investing in businesses at all stages of startup growth. Because the companies that VCs help fund hold little to no physical assets or inventory, nominal accounts receivable, and are cash burning (inhibiting their ability to service debt capital), they often have a hard time qualifying for traditional forms of financing, such as bank loans.

“Venture capital has played a key role in fueling technological innovation, supporting job growth, and establishing a strong knowledge-based economy in Canada.”

“Venture capital has played a key role in fueling technological innovation, supporting job growth, and establishing a strong knowledge-based economy in Canada. Equally as important—the top venture capital funds, typically those performing in or above the top quartile for their given vintage year, have produced strong risk-adjusted returns for their investors,” says John. “Without access to this type of capital, our Canadian innovation ecosystem would be nowhere near as strong as it is today.”

Venture capital vs. private equity

Private equity (PE) is defined as capital directly invested in private companies and includes a range of investment strategies. Venture capital is one type of private equity; however, the majority of PE is invested in established businesses, not early-stage startups. A typical PE investment strategy is to take a controlling interest in a business, play an active management role to increase its value, and then sell the investors’ stake for a profit. Compared to venture capital, private equity is typically a:

- Lower risk investment given traditional PE targets are typically mature enterprises with lower levels of return volatility

- Lower relative return investment compared to an early-stage investor in a breakout tech company

- Shorter held investment given the liquidity path being sooner for mature vs. startup companies

- Because of the high failure rate among startups (otherwise known as mortality rates), venture capital investors expect to see many of their investments go to zero. This is part of the reason as to why venture capital and early-stage investing is considered a ‘riskier’ asset class altogether

Venture capital vs. debt

A venture investment is provided by an investor in exchange for preferred equity in that company with no pre-determined repayment terms. Therefore, it’s viewed much more favourably than the traditional interest-plus-principal terms of traditional debt financing from a financial institution. As a result, venture capital acts as the primary source of growth capital for private companies, especially given the limited qualification pre-profit, cash-burning tech companies have in securing debt.

To complement venture capital, venture debt was rolled out to address the lack of debt financing available to the tech industry at large. Venture debt is a type of loan offered by select tech banking institutions and non-bank lenders to early or growth-stage startups that have successfully completed a prior venture capital raise. Venture debt is meant to bolster growth and extend operating runway. It’s structured like a term loan with a schedule of payments and typically doesn’t dilute ownership, but comes with a nominal warrant position that may impact company ownership, if exercised.

Who are the key players in venture capital?

Three key stakeholders are central to the workings of venture capital. Understanding the role of each helps clarify how this asset class operates in the innovation economy. The main stakeholders are:

- Company founder

- Venture capitalist (VC)

- Limited partner (LP)

The role of company founders

The venture capital ecosystem would not exist without the entrepreneur. Startup founders with big ambitions inevitably need capital partners to help their companies grow and cover cash-burn. So, it’s the founder who initiates the VC process by pitching to investors and choosing to partner with venture capitalists to fuel their company’s journey.

“Founders are at the core of the entire venture ecosystem. They are bold enough to bet on themselves and their team, and have an underlying ambition to build a fledgling start-up into an established, well-known enterprise,” says John.

The role of venture capitalists

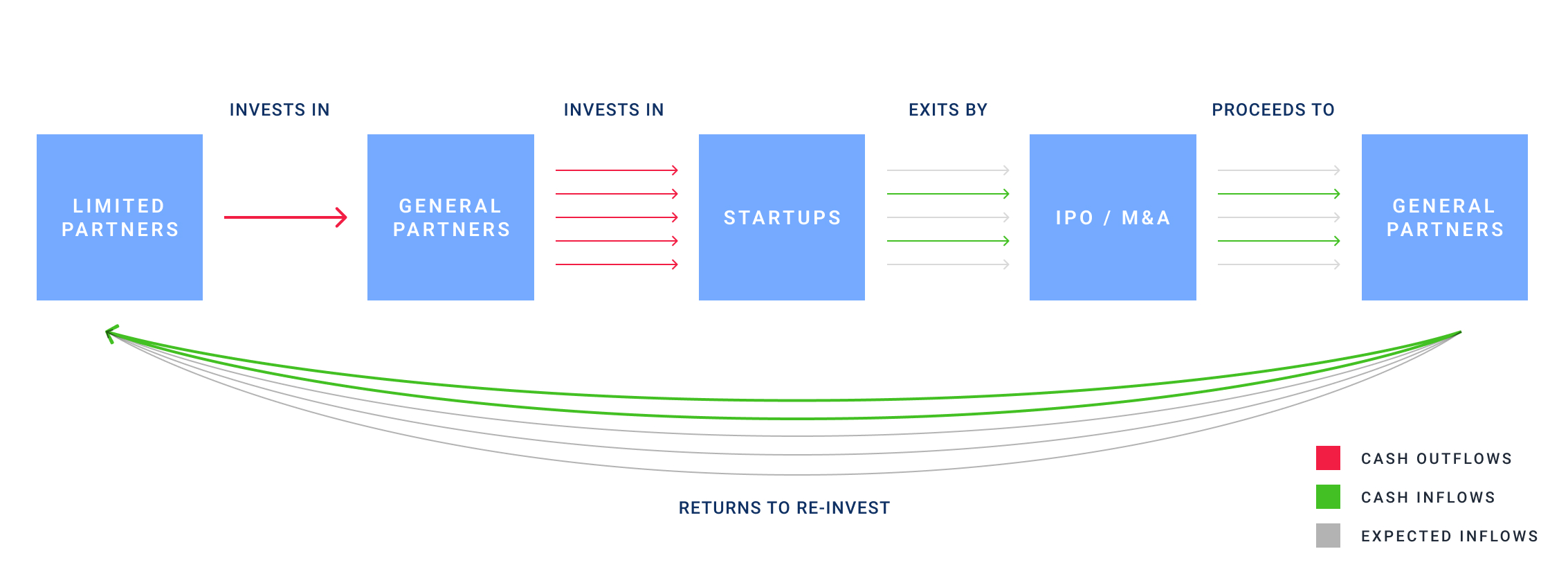

The role of venture capitalists is to provide capital and support to companies they believe have an outsized chance of becoming a market leader. A general partner (GP) is the most senior position at a venture capital fund, responsible for making and managing investment decisions of their firm. Ultimately, the role of a GP and a VC are one in the same, though “GP” is used in the context of a venture capital fund and “VC” can be used either within a fund or as an individual investor. As these venture investors build their portfolio and witness a select crop of their investments mature into established enterprises, searching for a path to liquidity (i.e. exit) will become the priority.

A general partner is the most senior position at a venture capital fund, responsible for making and managing investment decisions of their firm.

“Typically, the three primary liquidity off-ramps for private investors are a public offering, company merger or acquisition, or a secondary offering,” says John. For the select few VC-backed private companies that can achieve an exit, venture investors have one last role to fulfill prior to closing the investment—to return the appropriate portion of the realized proceeds back to those who initially invested in their fund, otherwise known as their limited partners or LPs.

The role of limited partners

Have you ever wondered how some venture capitalists have so much capital at their disposal? Just as startup companies seek capital from venture investors, VCs also undergo a fundraising process to raise capital from LPs to formalize and roll out their own venture capital fund.

“Limited partners can take the form of endowments, foundations, pension funds, insurance companies, family offices, fund of funds, and corporations.”

“Limited partners can take the form of endowments, foundations, pension funds, insurance companies, family offices, fund of funds, and corporations,” says John. “They are viewed as the money behind the money.” LPs deploy capital into venture capital funds that are managed by GPs. VC funds may target companies in specific industries, geographies, startup stages, or social causes, such as women-owned businesses or companies that develop technology to tackle climate change. RBCx is a proud LP in some of Canada’s most promising venture capital funds in areas spanning information, communications, and technology (ICT), life sciences, and climate.

Why do startups seek venture capital?

While some founders can build their startups without relying on venture capital, many need external funding to scale operations and achieve their target growth milestones. Given venture investors inherently take on equity risk with no formal repayment required of company founders, venture capital can be considered highly valuable to entrepreneurs in exchange for a loss of some control and ownership. Stated differently, the difference between owning 10 per cent of a $500 million dollar company and 50 per cent of a $20 million dollar company is $40 million dollars. “This has traditionally been the allure of venture capital,” says John. “With more capital raised, a company’s valuation rose in tandem.”

Founders may be motivated to utilize venture capital to:

- Launch a venture off the ground and establish the foundations of the company

- Fuel a company’s growth and capitalize on its early traction

- Prioritize growth initiatives to secure their market position against the competition

- Leverage the expertise and partnership of a top venture fund, its team, and networks

- Surround the business and management team with financially incentivized individuals all driving towards the same outcome (an exit)

Why VCs invest in startups

Venture capitalists invest in private companies that demonstrate high growth potential and an ability to produce an outsized return for their fund, which directly flows to their own investors. Since most companies (especially early-stage) have little or no financial history, VCs accept the substantial risk that comes with their investment.

“Venture capital is known to be a power law driven asset class whereby 20 per cent of the companies will generate 80 per cent of the returns.”

While in some instances, the risk pays off with a highly successful IPO (every VC is looking for the next Meta or Google), startup mortality rate is high. As a result, venture capital investors tend to invest in a portfolio of companies with the expectation that only a small subset will make up the terminal fund returns. “Venture capital is known to be a power law driven asset class whereby 20 per cent of the companies will generate 80 per cent of the returns,” says John.

Venture capital investors may be motivated to launch a capital fund and become a general partner to:

- Increase the total capital available for them to invest on behalf of their LPs, ultimately leading to a larger management fee and potential profits

- Leverage their superior skill set in sourcing, picking, investing, supporting, and exiting a portfolio of the most promising private companies

- Earn a strong (risk-adjusted) return for their LPs and be financially rewarded through their portion of the profit sharing (also known as “carried interest” or “carry”)

- Become an entrepreneur and establish the inaugural fund I of a long-term investment firm

- Control the deployment of capital in a specific area of value, such as newcomer entrepreneurs, geographic regions, climate change solutions, or other impact initiatives

Limited partners may be motivated to invest in venture capital to:

- Add further diversification to a portfolio of public and private equities

- Invest in venture capital funds that have the ability to perform in the top quartile or decile of their vintage year (the initial year that capital is deployed for investment) and thereby produce a strong illiquidity premium relative to public markets

- Leverage a GPs ability track record in being able to source, pick, invest, support, and exit a portfolio of top private investments

- Fulfill both the financial and strategic mandates of their enterprise

- Allocate venture capital on a more risk-adjusted basis through a fund’s basket of portfolio companies rather than invest directly in standalone private companies

How a VC fund operates

Founders should be familiar with the basics of how a VC fund is created, managed, and closed. Here’s a useful breakdown:

Establishing the VC fund

Before VCs can invest in startups, they need to raise capital from LPs to establish their fund. “Broadly speaking, a few areas that a GP would cover off with prospective LPs in the fundraising process would include team composition, fund strategy, capital allocation strategy, track record, and fund terms,” says John.

The agreement between the LP and GP, known as the Limited Partnership Agreement (or LPA) is structured as a 10-year term, with the potential to be extended. The GP needs many years to invest and allow their investments to grow into companies able to produce fund-level returns. The typical fund is structured as “two and twenty,” as follows:

- Two per cent (per annum) of the total committed capital is paid by the LP to the GP to manage the fund

- Twenty per cent of the profit sharing proceeds are allocated to the GP, and 80 per cent to the LPs

It is important to note, before the GP can share the realized proceeds (profits) from the underlying fund investments, the GP must first return to LPs 100 per cent of their original commitments.

Example of a GP fund’s fee structure:

A VC raises $100 million from 20 LPs who commit $5 million dollars each.

20 LPs x $5 million = $100 million

The agreement between the limited partners and the venture capitalist is structured as a 10-year term. The GP charges 2% per annum to manage the fund, and the fund’s gains will be divided 80/20 in favour of the LPs at the end of the 10 years.

This means 20% of the total fund commitment goes to management fees (10 years x 2% per annum = 20%), therefore, the LPs pay $20 million in fees on the $100 million fund over the 10 years, regardless of its performance. This results in the GP deploying only 80% of the fund into building the portfolio, equal to $80 million of total investable capital.

The three phases of a VC fund

Once the GP completes fundraising and the LPA is signed, they can begin to build the portfolio and source companies to invest in. Funds with a 10-year term can be broken down into three main phases:

Investment Stage – Years 1–3

The GP is responsible for deploying the initial capital into the underlying portfolio companies. A deployment period of three to four years is typically expected to ensure adequate time diversity across the deployment years. However, it can be accelerated to under two years if capital is cheap and abundant. Sound familiar?

Supporting Stage – Years 4–6

The GP is responsible for making any follow-on investments (if applicable) and supporting the underlying portfolio companies scale. In this period, dispersion begins to show in the underlying portfolio and the GP starts to concentrate on the top performers, rather than supporting companies that inevitably won’t make it to their target state.

Harvesting Stage – Years 7+

With a 10-year term, GPs begin to think about exiting their investments many years ahead of time to ensure the appropriate exit strategy is in place. In the last third of the fund life, the GP typically begins to crystalize liquidity paths to ensure capital can be returned to their investors at their agreed upon time frame, without jeopardizing investment performance. With companies staying private longer, fund terms may be extended beyond the 10-year term if agreed upon by the fund’s Limited Partnership Advisory Committee (LPAC). For the small handful of portfolio companies that do have an exit, the GP is responsible for receiving the exit proceeds and distributing them to the LPs.

Example of the end of a VC fund:

At the end of the 10 year-term, the $100 million fund (from the example above) has realized $200 million in investment proceeds. The LPs receive their initial $100 million back first.

The GP’s share of the remaining $100 million in profits is 20%, earning them $20 million. The LPs’ share is 80%, earning them $80 million.

Therefore, on a $100 million fund with $200 million worth of exits (2.0x), LPs leave with $180 million and GPs leave with $20 million.

For LPs, the goal is to receive distributions from their venture capital funds, and then continue to deploy in subsequent funds. This ensures that they are getting exposure to the diversified vintages with different deployment periods to improve the chances of investing in a fund whose portfolio may have the next Airbnb, Uber, or Meta.

“The cycle of raising capital, deploying capital, supporting the portfolio, and generating an exit to distribute capital back, then re-investing in subsequent funds, is how the venture capital ecosystem is designed to optimally work for founders, general partners, and limited partners,” says John.

A typical VC lifecycle

What’s a typical venture capital investment process?

As a founder, the process to acquire venture capital tends to follow a typical sequence. While many businesses may have the opportunity to pitch to VCs, very few tend to progress through the entire investment process. “Although a GP or venture fund may meet with hundreds or thousands of companies annually, their investment rate may be in the low single digits or potentially even below one per cent,” says John.

Below is a typical venture capital investment process for a startup that successfully receives venture capital:

- Sourcing: GP finds a company that they are interested in

- Initial meeting: The company pitches their company to the GP for consideration

- Evaluation/Diligence: Initial screening and diligence is performed to assess the founding team, market dynamics, business model, value proposition, use of proceeds, and target terms/price. There are multiple discussions in this stage

- Partner meeting: The lead GP prepares to present the Investment Memorandum to the partner meeting at the fund, and to align on next steps based on the investment committee outcome

- Final diligence: Final confirmatory due diligence is completed, including pricing, investment terms, investor syndicate, governance rights, and other areas prior to signing

- Signing: The GP signs the term sheet to commit to the deal

In anticipation of a deal being signed, a venture fund would “call capital” from their LPs, as they would only then require the necessary funds to complete the investment. Calling capital is the formal process by which a fund notifies their LPs to provide their pro-rata share of the target capital call amount, within a certain time—typically 60 days. The majority of the fund’s committed capital is called within the initial four to five years of the fund term when the fund is actively deploying the majority of the capital in building the underlying portfolio.

Expectations of startups that take on venture capital

Once the deal is signed and the capital is transferred from the fund to the company, the partnership between the fund and company officially commences. As shareholders of the company, VCs have a say in how the business is managed, however the level of active involvement will vary from one VC firm to another depending on their fund strategy. GPs often provide valuable support in areas including (but not limited to) corporate governance, go-to-market, business development, team building, executive recruitment, compensation structuring, and financial reporting.

With the fresh injection of capital, startups can expand their operations, hire top talent, invest in product and growth initiatives, and further establish their market position. Because VCs expect a high return on their investment (given the risk that comes alongside early-stage investing), there has traditionally been tremendous pressure placed on the company to constantly scale, learn, iterate, and expand operations.

“With capital being less widely available as it once was in years past, the previous ‘growth at all costs’ mandate has since been relieved in favor of capital efficient growth.”

“With capital being less widely available as it once was in years past, the previous ‘growth at all costs’ mandate has since been relieved in favor of capital efficient growth,” says John.

What startups should consider when seeking venture capital

If you’re a founder considering venture capital for the first time, the process can be a steep learning curve. From understanding new terminology to crafting the right pitch and researching VCs, the road to your first successful equity round likely won’t be easy. There are a number of ways to help ensure your business acquires the startup funding it needs to expand and enter into a fruitful partnership in which there is clarity and alignment on the direction and vision of the company for all parties.

Understand the VC business model

“One of the widest gaps I see in the current ecosystem is the lack of understanding, by founders, on the business model of venture capitalists and their incentives as fund managers,” says John. “As a result, founders may enter into partnerships with VCs without having a strong understanding of their underlying incentives and expectations. Moreover, founders may waste their time trying to reach an investor that is ultimately not a fit for their business to begin with.”

Consider that an early-stage investor will typically underwrite an investment by a standalone multiple, such as 10x to 50x target on their initial investment, or as a multiple of their fund, such as 1.0x. However, the reality is that most of their early-stage investments will go to zero. Understandably, VCs set incredibly ambitious targets for the founder. So, while the founder may be ecstatic with a $25 million, $50 million, or even $100 million exit outcome, it could be perceived as a non-ideal outcome to many VCs.

To ensure full alignment before entering a partnership, John recommends founders understand the following areas prior to taking on an investment from a VC:

How many investments does the fund plan on making?

Their number of investments and team size indicates how much value and support they’ll be able to provide your company. For example, a fund building a concentrated portfolio (that holds a relatively small number of investments) will likely have more time and a greater responsibility to support investments than a fund building an index strategy of hundreds of companies.

How much capital does the fund allocate between initial vs. reserve capital?

This will tell you if there is potential for the VC to further invest in your company should you hit your required growth milestones.

How are follow-on financing decisions made across the portfolio?

This should give you an understanding of what metrics to focus on to ensure capital is available for your company’s next raise, if required.

Where is the fund in their deployment period and how many net new investments do they have remaining to complete?

Though a fund may be $100 million in size, there’s a chance that you may be speaking to the fund in their final year of their deployment period and they only have a few initial investment slots remaining.

Build a trusting partnership

The relationship between founder and investor is best viewed as a partnership. For founders who still own a majority of the company, a VC investor will be their first official equity partner on the cap table. Founders need to feel comfortable challenging, collaborating, and ultimately trusting that individual or team. It’s essential founders understand where the VCs will focus their time and where they’re most impactful at adding value if that’s core to their strategy. Also know their reputation in the market for being high-impact partners.

Prioritize partnership over valuation

For startups that have multiple term sheets on offer, choosing the VC investor that will be the most strategic partner is often more important than selecting the investor offering the most capital on the best terms. It’s increasingly important, especially in this current market, to choose the partner you believe will be the highest-impact strategic partner for your business, rather than the investor that simply offers you the most capital.

As companies have raised multiple rounds of capital prior to a liquidity event, staying lean and capital efficient is in the best interest of preserving a founder’s own financial upside. It’s equally important to understand exactly how much capital you need, what the capital injection will bring to the business, and how the capital will build the business to a much stronger position from hitting target milestones. Investors who pile in capital during bull markets, only to go completely silent when times are difficult, are the types of investors to avoid.

RBCx offers support to startups in all stages of growth, backing some of Canada’s most daring tech companies and idea generators. We turn our experience, networks, and capital into your competitive advantage to help you scale and make a meaningful impact on the world. Speak with a RBCx Advisor to learn more about how we can help your business grow.

RELATED TOPICS

Other articles you may be interested in