A term sheet outlines an investor’s offer, intentions, and requests after a financing round and acts as the foundation for the formal legal documentation that follows.

Key points

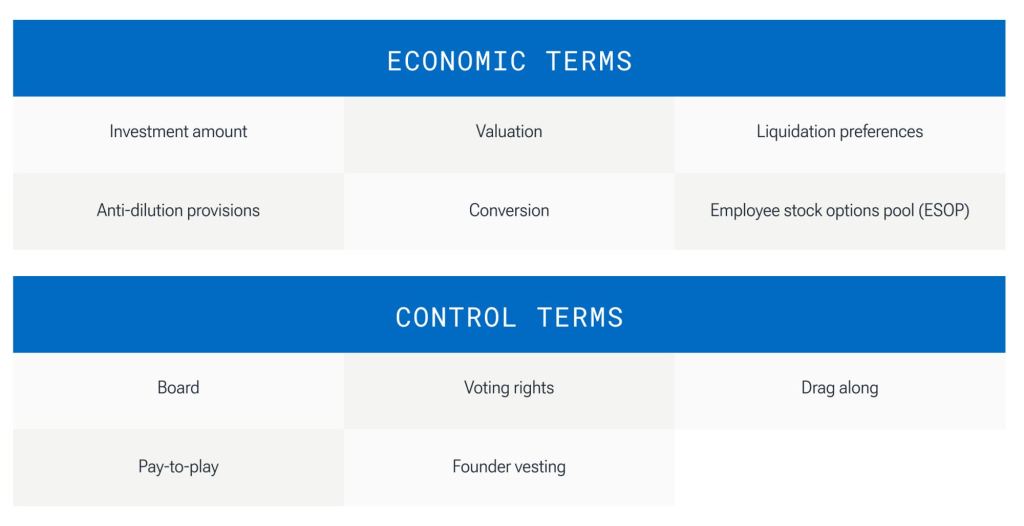

- The two main components of a term sheet are the economic terms that describe the financial details of the financing, and control terms that relate to the level of power investors will exert on your startup.

- Not every term sheet will require negotiation, however founders should be aware that an equity term sheet will often set a precedent for subsequent rounds. If the first term sheet is not founder-friendly, it may have a negative compounding effect over time.

- Founders may need to balance their negotiating aims, such as a higher valuation, with the desire to close a deal that has the potential to add tremendous value to their company.

A term sheet is typically the starting point for negotiation between founder and investor

For an early stage startup, securing an equity investor is a major milestone that helps fuel growth and provide valuable expertise from knowledgeable investors. But, before the deal is finalized, a term sheet is drawn up that outlines the investors’ offer, intentions, and requests. Typically, this non-binding proposal is the starting point for any negotiation between the founder and investors, and will act as the foundation for the formal legal documentation and due diligence that will follow.

Term sheets are often led by a lead investor and usually include multiple smaller investors in the same financing round. The lead investor is the investor committing the largest amount of capital to any given funding round. Once the term sheet is finalized and due diligence is complete, these terms and conditions will be included in a legally binding shareholder agreement.

Founders that clearly understand what is a term sheet and how its terms can impact their startup will be better equipped to negotiate founder-friendly terms. A fair term sheet can help create a mutually beneficial partnership between founder and investors, as well as set the foundation for future funding opportunities.

Components of a term sheet: economics and control

While there are many terms included in a standard venture capital term sheet, most of them fall into one of two aspects of a deal: economics and control.

- The economic terms of a term sheet describe the financial details of the financing, such as the amount of money to be invested, the shares the investors will receive, and any other attributes, including dividends, liquidity preferences, and more.

- The control terms relate to the level of power the investors will exert on the business, such as board representation and voting rights

This article describes commonly used economic terms and control terms found in a standard investment term sheet to provide a basic overview for founders going through their first successful funding round.

Economic components of a term sheet

Investment amount – This is the dollar amount the investors will provide the startup once the deal is confirmed and funded.

Valuation – This dollar amount quantifies how much the company is worth. The valuation is described using two different terms: pre-money valuations and post-money valuations. A pre-money valuation is the amount investors are willing to pay for shares of the business before the funds from the investment have been received by the company. The company’s price per share is calculated by dividing the pre-money valuation by the company’s outstanding shares prior to the round. The post-money valuation is what the company is worth after the round and is equal to the pre-money valuation plus the total of funds from the investment.

Liquidation preferences – A liquidation preference provides the investor who has preferred shares with an additional return on top of their investment when the company exits. The most common term is 1X their investment, but can be 2X, or higher, which would mean the investors can potentially get double or more of their money back. This term can significantly affect the founder’s return since preferences are paid out before the common shareholders or any lower classes of shares receive anything. There are three types of liquidation preferences:

- Non-participating – In a liquidation event, the investor has the right to receive the greater of: their preferred share value if they were to convert their shares to common shares, or the amount of liquidity preference specified of their class of shares (i.e. 1X their investment).

- Capped participating – In a liquidation event, the investor will receive their liquidity preference multiple plus they get to convert into common shares and participate on a pro-rata basis in the remaining proceeds. This is capped once they reach a target aggregate amount of capital returned (i.e. 3X their investment).

- Fully participating – Provides the investor with both a multiple of their investment amount (liquidity preference) plus the right to convert to common shares to receive their converted ownership percentage of the remaining proceeds, without any cap.

Anti-dilution provisions – This term is typically included to protect the investor’s investment when a subsequent financing is completed at a lower valuation, referred to as a down round. Anti-dilution terms prevent the ownership dilution that would occur with a financing at a lower valuation by giving the (initial) investor additional shares (at no cost) to maintain their ownership percentage even after the next financing round has closed.

Conversion – This term allows investors to convert their preferred shares to common shares, typically at a 1:1 rate. The conversion rights in the term sheet may be optional (at the discretion of the investor) or automatically triggered in certain circumstances.

Employee stock options pool (ESOP) – Used to attract and retain employees, an ESOP gives employees equity in the company by allocating a percentage of its shares to employees at no cost to them. An investor may mandate the company to top up its ESOP to a specific threshold, or to create an ESOP if one doesn’t exist before closing the financing round.

Control components of a term sheet

Board – This term defines the level of representation the investor will have on the board of directors. A founder-friendly structure provides a majority of board seats to founders, with the remainder being allocated to investors or independent directors. However, investors may include a structure that allocates the majority of board seats to them as part of their investment in order to exercise control of the board.

Voting rights – Investors often negotiate preferred shares with voting rights that provide protection and allow participation in major decisions. This helps create a balance between founder actions and the investors’ ability to have significant influence over decisions. In certain circumstances, this may even provide the ability to block the actions of founders or management that don’t align with investors.

Drag along – This term requires minority shareholders to follow the will of the majority shareholders in certain circumstances, such as the sale of the company. This prevents a minority shareholder that may have a very small ownership interest in the company from delaying or preventing a decision or transaction that is supported by the majority.

Pay-to-play –These provisions can have a large effect on the ownership structure and the rights and privileges of investors. Essentially, this clause requires investors to continue investing in a future funding round to maintain their ownership stake. There are many variations of pay-to-play so it is essential that both founders and investors understand the mechanics to the clause being proposed and how it may affect their ownership.

Founder vesting – This gives founders a certain number of shares or per cent ownership in a company that they earn over time. Founder vesting is established to incentivize founders to remain at the company. The schedule for founders to earn additional ownership is established prior to, or at the time of investment, and then earned over a number of years, usually three to four.

Common terms in a VC term sheet.

Insights and tips for negotiating a term sheet

While not every term sheet will require negotiation, founders should be aware that an equity term sheet will often set a precedent for subsequent rounds. That’s because new investors may expect the same or better terms than their predecessors, so if the first term sheet is not founder-friendly, it could have a negative compounding effect over time.

That being said, founders may need to balance their negotiating aims with the desire to close a deal that has the potential to add tremendous value to their company—especially if there’s only one offer on the table. Here are some factors to consider when negotiating fair terms.

Think long-term before negotiating a higher valuation

Although a lower valuation means more dilution of ownership for founders, it’s useful to remember that aligning with VC investors that add significant value can ultimately outweigh an investor that agrees to your valuation, but provides limited value enhancement. In addition, a singular focus on high valuation can impair the ability to raise future equity rounds as new investors may be reluctant to provide a significant valuation increase, and existing investors push for minimum dilution.

Understand how liquidation preferences can affect the founder’s return

Liquidation preferences can significantly affect the founder’s return since preferences are paid out before the common shareholders receive anything. In standard term sheets, non-participating preferences are the most commonly used, meaning the investor has to choose between taking their liquidation preference or converting to common shares and taking their fully diluted percentage of the proceeds. In some instances, investors may require more than 1X their investment back upon liquidation.

To determine the rationale behind a proposed liquidation preference, and whether it is appropriate, founders need to engage in discussions with potential investors to find what is driving the liquidation preference amount. Sometimes, and particularly in difficult markets, there may be a trade-off between pre-money valuation and investors requiring downside protection in the form of enhanced liquidity preferences.

Board representation can significantly influence your company’s governance

Investors typically add board representation to a term sheet to protect their investment by having a say on major business decisions. A structure of 2-1 (two founders and one investor) is more founder-friendly than a 2-2-1 structure (two founders, two investors, and one independent) in which founders have a higher risk of losing control over the business, and may even be fired by the board.

Solicit legal advice from a lawyer with relevant experience

Experienced lawyers will be able to explain all the mechanics of various provisions, as well as offer perspective on whether the proposed terms are similar to others they are seeing in the market. Founders should seek out the advice of an experienced lawyer to ensure they fully comprehend the implications of the term sheet.

Adopt a holistic view when there’s more than one offer on the table

Multiple term sheets will require careful consideration. Avoid focusing on one metric, such as valuation. All the terms, conditions, and valuation should be considered holistically. There may be trade-offs required, but finding a balance that supports growth without placing onerous conditions on the company is the key.

Focus on creating a great relationship with the investors

Founders should understand that investors will be their partners on an ongoing basis. Therefore, looking beyond quantitative factors, such as valuation, helps ensure a productive and transparent relationship with investors.

It’s important to keep in mind that the deal is not closed until after due diligence and legal documents are signed (so, don’t count your chickens before they’re hatched.) As you consider and execute your negotiations, remember the investor is there to support your growth—closing the deal will help fulfill your vision for the company, which may be more important than negotiating your ideal term sheet.

Term sheet Q&A

What is a term sheet?

A term sheet outlines the overall deal and key requests of an investor that is drawn up prior to finalizing an investment in a startup. Term sheets are also drawn up by banks for borrowers to outline the terms of a loan.

Is a term sheet a pre-approval?

A term sheet acts as a blueprint for the legal documentation that will finalize the deal, but it is not a commitment or obligation to move forward with the investment for either party, nor is it legally binding. A term sheet provides the basis for negotiation between the founder and investors to help ensure both parties are aligned on the significant terms of the financial arrangement to proceed with the due diligence.

Are term sheets usually signed?

Term sheets may be signed to indicate agreement on the provisions between the two parties. However, a signed term sheet does not make the proposal legally binding.

Is a term sheet legally binding?

A term sheet is not legally binding. It provides the foundation for the legal documentation that will follow once the agreement is finalized.

Is a term sheet negotiable?

Founders can negotiate the terms of a term sheet to ensure the deal is mutually beneficial to both the VC and the startup. In some cases, a founder may be presented with multiple term sheets which can provide leverage for negotiating the most founder friendly terms. However, too much negotiation may put the deal at risk, which is something every founder needs to consider when prioritizing which terms to focus on.

RBCx offers support to startups in all stages of growth, backing some of Canada’s most daring tech companies and idea generators. We turn our experience, networks, and capital into your competitive advantage to help you scale and make a meaningful impact on the world. Speak with an RBCx Advisor to learn more about how we can help your business grow.

RELATED TOPICS

Other articles you may be interested in